Emerging Debt Trends in Asia Pacific

The credit environment across the Asia Pacific region continues to shift towards a more homogenised model within the traditional lending base. As banks move towards increasingly selective, conservative credit terms within the region, more flexible forms of finance are coming in to fill the void.

Post the financial crisis, traditional lenders have faced increased banking sector regulation, as well as more stringent risk management parameters applied internally by credit committees. This has led a large wave of capital working towards the same lending parameters, and has created price pressure for core assets that fit a well-defined set of loan criteria. Some investors that have an excess of equity raised or are long-term passive investors with lower return hurdles are now also seeking to utilise lower levels of leverage. This is compounding the difficulties facing banks as they seek to extend credit in an overcapitalised segment of the market that has less appetite for their credit.

One of the key drivers behind these difficulties is the impact that real estate lending has had on banks’ capital requirements. Banks have had to set in place higher capital adequacy requirements to manage riskier lending practises, however these have reduced the banks’ net interest margin for these types of loans.

Outside the core investment segment, leverage ratios and term maturities are under pressure and the availability of development finance has become more challenging to obtain, particularly for those without strong banking relationships. The subsequent lending gap is being filled by either more equity or higher cost forms of credit.

This is creating its own set of challenges as investors/developers are tipping more equity into their deals. This is reducing their ROE and deteriorating other denominator-based return metrics. On the other side of the equation, finance being sourced by debt/special situation funds is costly, as is much of the last-mile project finance and mezzanine debt being used by developers.

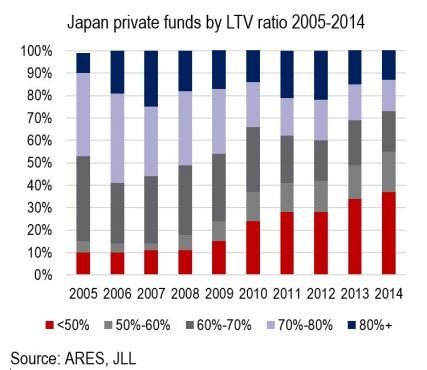

The chart below highlights the continuing trend toward lower leverage utilisation by private funds in Japan. In 2007, just 14% of private funds had LTV ratios below 60%. As of 2014, that same figure is over 55%.

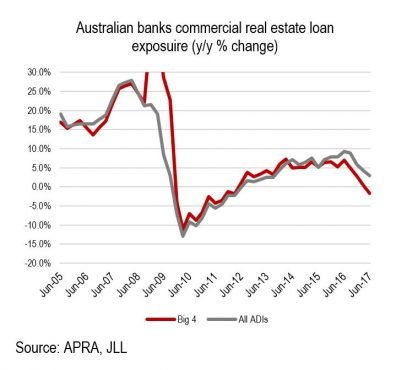

Regulators are also now trying to understand the size and nature of these unregulated lenders. The Reserve Bank of Australia for example recently stated that tougher bank regulation has led to an increase in shadow banking. While there are no hard statistics on the sector, they believe as much as AUD 28 billion has been lent to developers via these channels. Australia’s Big 4 banks on the other hand have seen their exposure to commercial real estate actually fall (-1.7%) over the past year, with overall exposure by all Australian Depository Institutions (ADIs) growing at a much slower pace than the past few years.

While non-bank lenders can be very healthy for a financial system as they step in and fill a temporary gap, their long-term viability is less well understood. Their shorter-term outlook can also create systemic risks in some areas of the market.

There has been a slight shift across the region as more investors are looking at debt investment strategies. Private equity funds in the region specifically targeting debt strategies are likely to achieve a record year of capital raised in 2017, with most of these funds targeting residential development finance in India and Australia.

With so much capital targeting core debt and core equity, as well as a growing pool of investors operating in the more opportunistic debt space, there remains a funding gap between the core and opportunistic segments. Equity investors have seen core leverage rates tighten up over the years, creating a dearth of stretched-senior tranches in a number of markets. Banks tend to finance deals often up to around 50%, however that segment between 50-65% remains a relative “no man’s land.” Coupons in this segment of the market are also generally above core equity yields so there are strong returns on offer for investors looking at high yield product with a stronger level of downside risk protection (when compared to equity).

Is a complex credit market

good?