Migration deflation and its impact on Melbourne housing

In response to the COVID-19 pandemic, we’ve seen a freeze on interstate and international migration. What impact does this have on housing demand and our apartment supply pipeline?

Less migration means less demand for housing markets. In recent times, net overseas migration has been a key driver of house prices and underlying demand, particularly in Victoria. In response to the COVID-19 pandemic, we’ve seen borders closed to non-residents and a freeze on the interstate and international migration. What impact does this have on housing demand and ultimately our apartment supply pipeline?

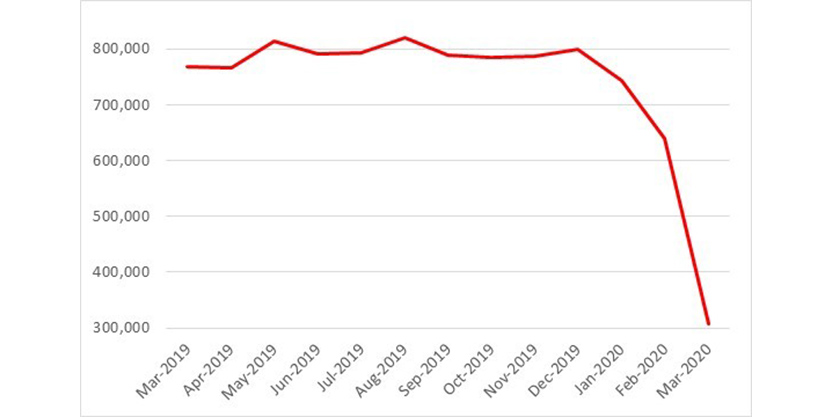

Figure 1: Australian short-term visitor arrivals (seasonally adjusted)

Source: Australian Bureau of Statistics (ABS), as at March 2020

ABS data showed a record fall (70%) in short-term overseas arrivals in March 2020. Federal Treasury expects a 30% decline in the net overseas migration this financial year and an 85% fall forecast for 2020-21. In recent years, temporary visa holders have been the dominant cohort of overseas arrivals, a significant proportion of these being international students. As such, the slowdown in migration will likely soften demand for housing. Moreover, we, expect the Victorian residential market, Inner Melbourne in particular, to be hit harder than other states due to its reliance on international education and tourism. However, the loss will go far beyond just international students, with migration playing a vital role in filling skill gaps across the economy with imported temporary and permanent migrants.

What impact will the decline have on Melbourne’s supply pipeline?

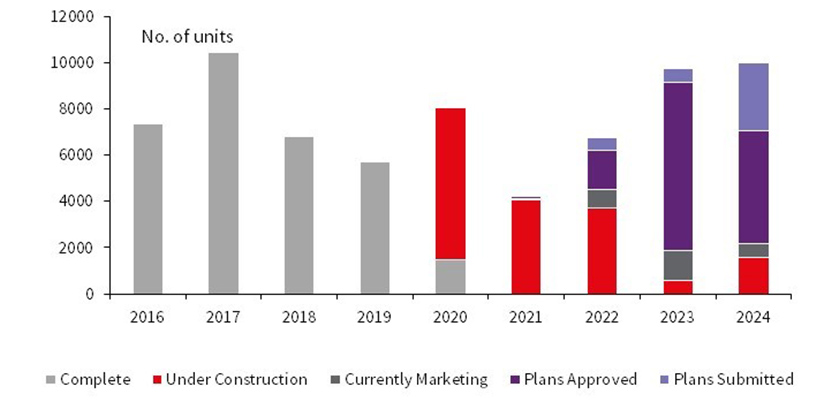

Migration and the international education market have been crucial in underpinning high levels of completions in the Inner Melbourne apartment market over the last five years. With this key driver now diminished for an indeterminate period, follow-on effects will likely continue to depress pre-sales demand and delay construction commencements. JLL research expects annual completions for Inner Melbourne to be total 8,000 apartments in 2020, dropping to 4,200 in 2021. More uncommitted projects are likely to be delayed, and construction could stay very low in at least 2022 and 2023.

Figure 2: Inner Melbourne Supply Pipeline

Source: JLL Research, as at 1Q20

With 16,400 apartments under construction in Inner Melbourne and 81% of these in the Melbourne City precinct, the fall in migration is likely to leave excess supply and have a detrimental effect on the Inner Melbourne sales and rental markets. However, in the medium-term, migration will eventually bounce back, with a lower AUD and only a moderate health crisis compared to other countries, and thus potentially making Australia an attractive destination for foreign investments and international students. When demand is back in full swing, there will be little new supply to meet this demand, and the market could tighten up relatively quickly.

Only a year ago, Scott Morrison announced a cap on migration, reducing it to 160,000 annually, from 190,000, effective for four years, citing that we had become a victim of our own success, especially Sydney and Melbourne. This reduction was in response to overcrowding and congestion concerns. Essentially, the COVID-19 crisis has exposed the need to find a happy medium with regard to migration. Not too many, not too little, but reaching economic equilibrium for the apartment supply market.

In the meantime, what we don’t know is exactly when will this “migration deflation” cease, when will international borders reopen, and ultimately how long will the transition back to normalcy take?