Unlocking full potential of Hong Kong's office market

Despite the challenging market conditions, some potentialities may emerge.

In recent years, vacancy level has continued to edge higher across Hong Kong’s overall Grade A office market and in some decentralised submarkets. According to JLL, by the end of Q1 2024 the overall vacancy rate for Grade A offices in Hong Kong stood at 13.1% - the highest since the 1990s.

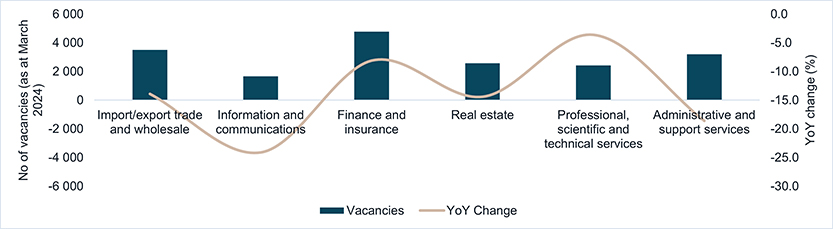

In Q1 2024, there were 18,160 job vacancies in office-related industries in Hong Kong. However, even if all job vacancies were filled, with each job position requiring 73 sq ft of net floor area (NFA), the market can only absorb 1.3 million sq ft of office space. With total vacant office space currently stands at 14 million sq ft, this would only help reduce the overall office vacancy rate to 12%.

To occupy this remaining 13.2 million sq ft of vacant office space, our analysis indicates the market would require at least 181,700 additional new office-related job openings. In summary, the 18,160 existing vacancies are insufficient to significantly reduce the total vacant office space.

Figure 1 - No. of office-related job vacancies in Hong Kong

Source: Census and Statistics Department, JLL, 2024

In the medium-term, the market will have to contend with high vacancy levels. However, even during broader economic or market challenges, there are bright spots that offer a measure of optimism over a longer timeframe.

The high vacancy levels give occupiers more flexibility to move to newer buildings, where they can leverage stronger bargaining power. In these market conditions, buildings that are newer, forward-looking, and incorporate ESG features as well as advanced technology will have a competitive advantage. This dynamic creates opportunities for both occupiers, who can be more selective, as well as landlords of the most forward-looking buildings, who can potentially maintain stronger occupancy and rental rates. It's a shift that favors modern, sustainable real estate assets over the medium to long term.

According to JLL APAC Research, the office re-entry rate has gradually returned to a 'normal' level. Specifically, Hong Kong's office re-entry rate has shifted towards the 'normal' (over 90% of normal) range over the subsequent years. This suggests that the city has since seen a steady return of employees to in-person work at office locations.

Additionally, the finance and insurance sectors in Hong Kong are poised to benefit from several key demand drivers in the coming years. Integration within the Greater Bay Area (GBA) and Hong Kong's role as an offshore RMB hub presents a significant opportunity for the industry. Hong Kong's status as a leading international financial centre, combined with the fundraising needs of China's burgeoning tech sector, is expected to generate sustained demand for financial services, thus translating to sustainable office demand

On the other hand, Mainland China is set to remain a primary engine of global economic growth. This China-driven growth is also anticipated to boost demand for asset management and cross-border wealth management services in Hong Kong as investors seek to capitalise on the country's economic dynamism.

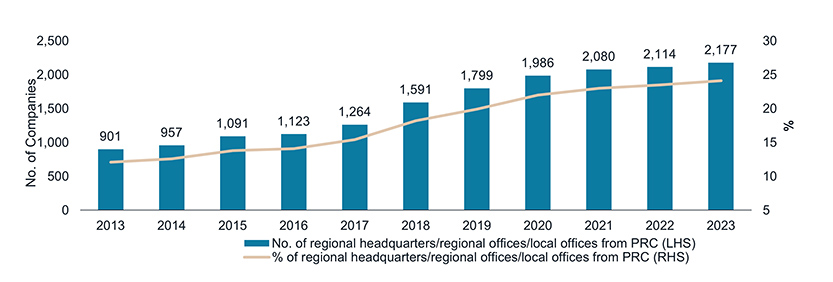

The chart below shows that the number of PRC offices has increased from 901 in 2013 to 2,177 in 2023, indicating a substantial expansion of over 140%. Moreover, the percentage of PRC offices in Hong Kong soared, from around 13% in 2013 to 25% in 2023. This consistent growth reflects the deepening economic integration and increasing business presence of mainland China in Hong Kong.

Figure 2 - No. of regional headquarters/regional offices/local offices from PRC in Hong Kong

Source: Census and Statistics Department, 2024

The continued presence of multinational corporations (MNCs) in Hong Kong provides a reliable source of sustained demand from non-local companies operating in the market. This diverse set of demand drivers, ranging from regional integration to domestic and international corporate activity, positions the finance and insurance sectors as key beneficiaries of the city’s ongoing economic development and evolution.