Will affordability support apartments in Australia?

The gap between apartment and detached house prices in Australia is currently wide, which should support apartment demand and price growth over the medium-term.

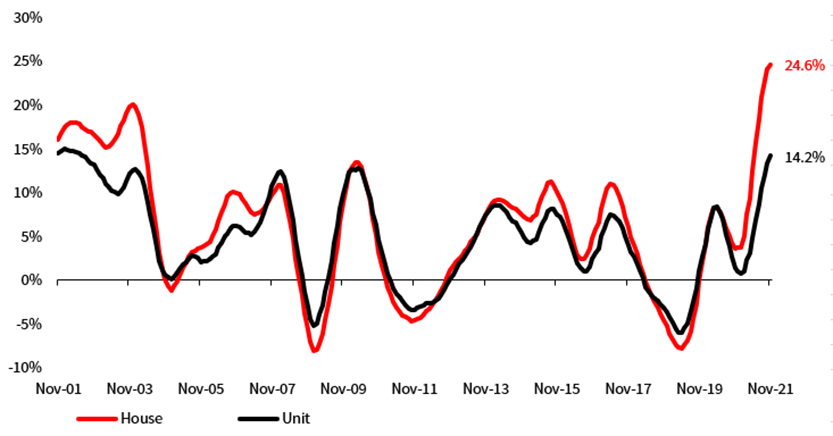

Australian apartment prices have grown strongly the past year (14.2% over the year to November), but this is only around half the growth seen in detached housing.

There are good reasons for this difference. The rebound in the housing market has been driven by a combination of record-low interest rates, fiscal incentives such as HomeBuilder, and first homebuyer incentives. All of these had a greater initial impact on detached housing demand, while the apartment market in many parts of the country (particularly Melbourne and Sydney) was also still absorbing the tail end of the last supply cycle.

As such, the gap between detached house prices and unit prices has widened. In November, the average difference between unit and house prices across the major capital cities was 37%, compared to 30% a year ago and over the past decade. The difference ranges from 27% in Perth to 43% in Canberra. The differential in Brisbane (41%) is also particularly wide and in all markets the gap is considerably wider than on average over the past decade.

Even though the affordability gap is wide in most markets, in some markets the affordability challenge is simply the price of detached houses, which is far beyond the reach of average income buyers. This is most clearly the case in Sydney where the median price of a detached house is $1.36 million, but also in Canberra and Melbourne that are both rapidly closing in on a $1 million median. Moreover, rapid escalations in greenfield land prices, strong rises in build costs, and the winding back of first homebuyer incentives have all pushed traditional ‘house and land’ packages well beyond the reach of most first homebuyers.

Figure 1: Annual Dwelling Price Growth (% p.a., 8 capital cities)

Source: JLL Research, CoreLogic, Nov-21

Figure 2: Comparison of Unit to Detached Dwelling Prices

Source: JLL Research, CoreLogic, Nov-21

There is already some evidence that these pricing pressures are pushing more demand back into apartments. We expect this pressure to intensify and become more relevant across all markets over the next few years.

When interest rates do inevitably rise, this will reinforce this trend even further and price more buyers out of detached housing. Regardless of when interest rates do rise, the measures already taken by APRA, and any further measures taken, to tighten borrowing assessment criteria will also reduce borrowing capacity and push more buyers back into attached dwelling pricing levels.

This additional demand support for apartments from an affordability perspective will also be added to by the opening of borders and the return of migrants and foreign students, plus a continued rise in investor demand. At the same time, new supply into the apartment market over the next few years will remain moderate. This will see any surplus apartment stock (particularly in Melbourne and Sydney) absorbed more quickly.

All of these factors together are likely to provide upward price pressures over the medium-term for apartments and support robust price growth over the next few years, even as detached prices stabilise. As such, we expect the pricing differential to narrow again over the next few years.